Groundhog Day?

Groundhog Day?

Fool me once, fool me twice -- fool me four times?

Several stories this last week have me just a little concerned about the oil renaissance that we’ve been experiencing so far in 2021.

The biggest concern with oil and oil stocks remains the same since we saw the first major ‘bust’ in prices in 2014: That the undisciplined and frankly desperate and over-leveraged shale oil specialists would take any opportunity to open the floodgates on their oil supplies to create much needed cash flow. This would again add to the global gluts of oil that have kept oil prices, and oil stock prices relatively low since then.

This cycling of mini boom/bust in oil prices and concurrently in oil stocks has happened by my count three separate times since that first one in 2014. And, despite this obvious self-destructive behavior of oil companies, they have never looked like they were going to get smart about over drilling, despite all their protestations to the contrary to both analysts and shareholders alike.

This time was supposed to be different, however – the decimation of the last mini-bust in the last half of 2019 led straight into the mega-disaster of the Covid-19 pandemic. Here was a case where so much of the potential production in the big Permian plays were either rolled-up, sold, restructured or otherwise moth-balled to a degree that it COULDN’T come back online fast enough to again screw up the work of the Saudis and OPEC+ and fast rising oil prices this year.

I still think that is the case – but to the degree that smaller shale players can open their spigots, now that Brent oil prices are above $60, they’re doing it --- and getting some help from the usual suspects.

The first is the investment banks, who have a habit of throwing a ton of good money after bad in the oil patch. Seems like they’re at it again, issuing a record amount of junk bonds in the first quarter of 2021, an estimated $20 billion – all for the same crappy drillers they (or actually their clients) have lost a fortune with in the last 7 years.

What is wrong with these guys?

I don’t blame the oil companies – I mean, I do – but really, they’re only looking to keep the lights on. The bankers, however, are looking to instead salvage their bad investments in teetering oil E+P’s, and using near-zero interest rates and the upswing of oil prices to try and do it. The shortsightedness of this kind of finance is not only breathtaking, it’s become pretty typical of IB behavior since, well, since 2007 and a much bigger finance problem.

Rig counts are going up. Depending on how you count it, it’s up 100 or so since the beginning of the year, still 30% below last year at this time, but a significant rise anyway. That’s all about oil prices, of course.

Brent backwardation of spreads has come in a lot – from about $5 to about $2. This means that traders have begun to think that the enormous 5m barrel a day supply shortfall that the IEA has been predicting (and oil companies have been counting on) is not going to be nearly as extreme.

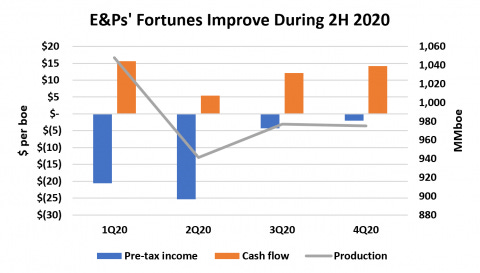

And then, of course, there’s production – still lagging early 2020 by a lot – but cash flow is rebounding awfully fast, and that always gets accompanied by barrels soon after. This is upsetting the complete comfort of guys like me, who’ve seen this ‘Groundhog Day’ repeating show play out over and over again in the last 7 years.

To sum up: Again, I’m still convinced that the rebound in oil isn’t anywhere near over. But you know the expression that ends “fool me twice, shame on me”? Well, what about getting fooled four times in a row?

I’m going to be very cautious and make sure that doesn’t happen under any circumstances – to me or my subscribers.